2021 Year end superannuation planning guide

We are pleased to provide our superannuation year-end planning guide for 2021.

Tax Planning should be done on a regular basis throughout the year. However, given the current economic circumstances and changing tax rates, these tips are especially relevant to consider just before the end of the financial year.

Outlined below are a number of suggestions that may assist taxpayers to legitimately minimise or defer their taxation exposure.

Please note these suggestions are of a general nature only should not be relied upon without seeking specific personal advice. We recommend that you contact your usual Mazars advisor to assist you with your own specific tax planning requirements.

While business owners should be reviewing their year to date performance regularly, if this hasn’t occurred now is the time to be doing it. Prepare up to date management financial statements and cash flows with comparisons with previous years and against budgeted performance. This should help to determine how the business has performed to date, the likely full year performance and will establish a platform for this year’s tax planning and future budgeting. This is especially relevant now as you need to understand the business’s current ability to move forward in the current economic circumstances and plan for the future.

During 2021, there was a continuation of unprecedented levels of stimulus provided to business by Government. Further, the delayed Federal Budget in October 2020 and the 2021-2022 Federal Budget provided new tax incentives.

The Base Rate Entity company tax rate will have a further and final drop from 26% to 25% from 1 July 2021 year. This creates arbitrage opportunities.

With the reduction in company tax rates, the franking credit rules will change. Any dividends paid must be franked to the same tax rate that applies to the company in the year that the dividend is paid. During the 2021 year there may be some leakage of franking credits if tax was paid at 27.5% but the dividends are required to be franked at 26%.

This is exasperated next year when the tax rate becomes 25%.

The receipt of the Cashflow Boost (refer below) is Non-Assessable Non-Exempt Income (i.e. non-taxable unfranked income) and will reduce the Franking credit trap.

Many businesses have received either a government ‘Cash Flow Boost’, Jobkeeper or other Government Grants.

Cash Flow boost is not taxable. If received in a company it can represent unfranked profits so is ultimately taxable when paid to shareholders. However, it should not be taxable if received by a sole trader, partnership or trust where these payments end up in the hands of individuals.

Jobkeeper payments are taxable but are offset by payments to employees so there should be no net taxable income.

Most other Government Grants will represent assessable income. However, certain State Government Grants are exempt, so you should check with your advisor. Most State Government stimulus resulted in a reduction in State Government payments. This will result in reduced deductions.

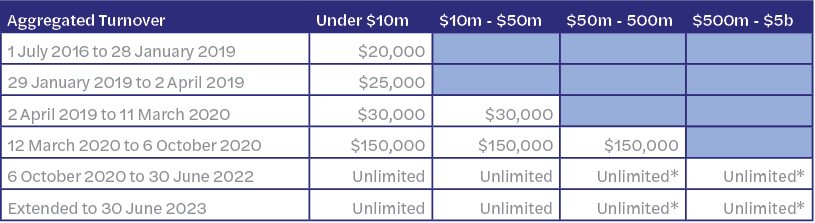

Over the last number of years, the Government has incentivised businesses to invest in assets by allowing them generous thresholds to write off the cost of an asset as a tax deduction in the year of purchase. This first applied to small business (<$10 million turnover), then medium business (<$50 Million turnover).

This then increased with Covid stimulus and then Budget announcements. The table below illustrates the changes in the incentive amounts and thresholds.

Instant Asset Write-Off Limit - Cost of Asset

Notwithstanding the provisions above, the depreciation limit for the cost of a car is limited to $57,781 for the 2021 income year.

A further ‘Backing Business Investment’ incentive was introduced from 12 March 2020 and running until 30 June 2021 for business with turnover of less than $500 Million. Where the above instant asset write-off did not apply, business could acquire a new asset and deduct 50% of the cost immediately, then normal depreciation rules apply to the remaining 50%.

This has mainly been replaced by the Unlimited instant asset write-off but may still have residual application for asset acquired prior to 6 October 2020.

There is a “temporary loss carry-back tax offset".

If a company made a profit and paid tax in the years ended 30 June 2019, or 2020, but had a loss in either of the 2020 or 2021 years, the tax offset allows the loss to be carried back to the income year. The resulting ‘refund’ that would be generated is allowed as a refundable tax offset in the 2021 year. This is only allowed provided there are sufficient franking credits remaining within the company to provide for the tax refund.

Refer to the Instant Asset Write-off rules above which currently apply to all entities.

Other small business concessions include simplified trading stock rules, GST and FBT rules and the ability to deduct prepaid expenses immediately.

Note most of these rules will be extended from 1 July 2021 to entities with turnovers of less than $50 Million.

In addition, if you have made a capital gain in relation to an asset used in your small business, various CGT concessions may be available. The turnover threshold for the concessions remains at $2 Million rather than

$10 Million. They are also available for small business entities and business taxpayers with net assets of <$6M.

If available, the taxpayer may be able to access:

Please talk to us before you consider selling your business to avail yourself of the best possible concessions. Tax planning ‘after’ the event is often less effective or not available at all.

If cash flow and business reality allow, consider deferring the derivation or receipt of income until the next financial year. This is especially relevant for companies with the change in tax rate. If on a cash basis,

consider trying to defer the receipt of cash. If reporting income on an accruals basis, defer the derivation of income by holding back invoices if possible until after 30 June.

Consider whether income received is actually derived. Income received in advance may not be derived (and not taxable) until the services are provided. Conversely income such as interest, royalties, rent and dividends are usually derived upon receipt.

Expenses are only deductible when incurred, i.e., there must be a presently existing liability to pay the expense. Many accruals and provisions are not deductible as they represent an estimate of expenses and do not relate to a presently existing liability.

Most prepayments now are not deductible until the period to which they relate (some exceptions apply), although small businesses and individuals may be able to deduct 12 months of prepayments in the year paid.

Businesses can only claim a deduction for payments to workers (employees, contractors, directors etc) where the business has complied with PAYG withholding and reporting obligations. If payments are paid but not correctly reported to the ATO, the business will be denied deductions, even if the individual correctly includes the amount in their income tax return.

This may mean some family businesses that may have paid wages or allowances to family members below the tax-free threshold will need to register as a withholder and provide a PAYG Summary, or process payments through Single Touch Payroll.

Most businesses should already now be using Single Touch Payroll. This extends to all business (including small family business) from 1 July 2021.

Review your debtors and if any are unlikely to be recovered, actually write them off as bad before 30 June. This will reduce your income tax and should generate a GST refund (for taxpayers registered for GST on a non-cash basis).

Prepare for a stock take on 30 June. Identify any obsolete or old stock and scrap it or write it down to its correct market value. Individual items of trading stock can be valued at cost, market value, or replacement value for tax purposes. The tax value may differ to the accounting value.

Bonuses are only deductible when they are actually incurred i.e. at 30 June the business must be committed to paying them and they are not subject to any discretion.

Note the special COVID19 asset measures discussed above.

Assets purchased during the year can be depreciated using the diminishing value method at 200% of the prime cost rate.

Review your asset register and scrap any obsolete items before 30 June. If you will be selling any items of plant that will realise a profit on sale, consider delaying the sale until after 30 June. Conversely, if selling assets that will realise a loss, bring it forward.

The Australian Taxation Office (ATO) considers (in administrative practice statement PS LA 2003/8) that items costing less than $100 can generally be claimed as deductible outright (some exceptions apply). All assets above this amount should be depreciated.

The ATO considers that only contributions that are received by a superannuation fund by 30 June 2021 on behalf of employees including working directors, are tax deductible to your business in the 2021 year.

Payment to a superannuation clearing house before 30 June may not be sufficient to guarantee deductibility as the clearing house needs to pay it to the fund. Accordingly, if you plan to pay all June quarter superannuation before the end of June, we recommend this be done as early as possible.

As 30 June falls on a Wednesday in 2021 we recommend that contributions are made in the week prior.

As noted above, Base Rate Entity companies (Aggregated business turnover of less than $50 Million for the 2020/2021 year and with less than 80% of income as passive income) will only pay tax at 26% of their taxable income (other companies 30%). If your company’s turnover is close to the threshold, consider income deferral strategies to reduce the tax payable. This tax rate reduces to 25% in the 2021/2022 year, so strategies to defer income will result in lower tax.

To get the 26% tax rate, a company must be a ‘base rate entity’ (refer above). Accordingly, companies receiving only passive investment income, or only receive distributions from a trust will pay tax at 30%.

We recommend you contact your Mazars advisor to discuss any planning for use of corporate beneficiaries.

Have you considered whether your company may be eligible for an additional tax concession for R & D expenditure undertaken?

If your company’s turnover is less than $20M, it can access a refundable tax offset equal 43.5% of the R & D expenditure. There is a 38.5% non-refundable tax offset available to companies with turnovers of greater than $20 million.

R & D plans need to be registered with The Department of Industry, Innovation and Science before claiming the concession. Cut off is 10 months after the end of the financial year.

Do you own > 10% of the shares or units in a foreign company or trust? If so have you considered whether the Controlled Foreign Company or other attribution rules will have application and attribute income to you?

If you have foreign transactions, have you correctly recorded any foreign exchange gains or losses under the Forex realisation rules?

Have you withheld and remitted non-resident withholding tax on payments of dividends, interest or royalties to non-residents? An annual report will be required.

Any payments, loans or debts forgiven from private companies to shareholders and their associates could be deemed to be an unfranked dividend.

The deemed dividend rules in Division 7A can also include deemed loans from trusts to shareholders where the company has an unpaid present entitlement (UPE) to income of the trust. Division 7A can also apply to the private use of a company’s assets by a shareholder (limited exceptions apply).

Action can be taken to prevent deemed dividends from occurring. Ensure that such loans are either repaid or documented and made subject to minimum interest and repayment terms before the lodgement day of the company / trust’s tax return.

Ensure that interest is charged, and minimum repayments are made before 30 June in relation to prior year loans.

When paying dividends or interest to non-bank lenders, there may be a requirement to complete a dividend and interest schedule.

After a company has paid a dividend, it must provide a statement to shareholders noting the amount that the dividend is franked.

In addition to the above business planning ideas, further ideas may be available for individuals and families with business or non-business income.

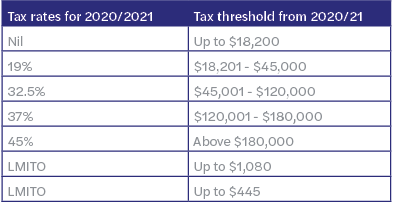

Resident Individual Tax rates are as follows:

Losses of a business carried on by an individual or partnership may be required to be quarantined until future years against income of that or of a similar / related business. The exceptions are:

In addition to the above, taxpayers with adjusted taxable incomes above $250,000 cannot use these tests and losses are quarantined until a year where income falls below $250,000.

CPBs are arrangements that protect an investors ‘capital’ against the fall in market value of a security against which they have borrowed. Usually the capital protection involves a higher interest rate on the loan.

A portion of the interest on loans that facilitate a CPB may not be deductible (to the extent of any capital protection premium).

If you are considering investing in any ‘tax effective’ investments, ensure they have been granted a Product Ruling which sets out the tax treatment of the income and expenses in relation to the investment as the ATO are continuing to scrutinise these investments. Always seek professional advice from an AFS license holder before investing in any financial products.

Investment in Early Stage Investment Companies (ESIC) provides a 20% tax offset (capped at $200,000 for $1 Million invested). Non-sophisticated investors may only invest a maximum of $50,000 to qualify. Capital Gains may also be disregarded if the shares are disposed after 12 months but before 10 years. Various criteria apply to ensure the company is an ESIC.

The employee share scheme rules are quite complex. Employees are no longer allowed to elect that they be taxed up front. Instead, they are either taxed up front, or taxed at a deferred taxing point depending on how the scheme is structured. Employers are required to provide employees with a statement advising of taxable discount of shares and options under such schemes.

Trustees of discretionary trusts need to consider which beneficiaries they will make presently entitled to the income or capital of the trust on or before 30 June.

The trust deed should be reviewed to consider how trust income is to be determined and to which beneficiaries’ income can be distributed.

Individual beneficiaries of trusts with aggregated business of less than $5 million can get a 13% discount (capped at $1,000 per individual) on the business income received from a trust.

Trust Distributions are a continued ATO focus, so care needs to be taken.

Mazars will be further providing guidance to our trust clients about trust distributions before 30 June.

We note that the tax legislation contains specific anti-avoidance provisions which target schemes entered into with the dominant purpose of tax avoidance. Accordingly, it is essential that you consider your specific circumstances before proceeding with any tax planning ideas to ensure these rules do not apply.

If you are a taxpayer on the PAYG Instalment system and you plan to use some of these tax planning tips to reduce your 2021 taxable income, you may be able to vary the June quarterly instalment (due 28 July) to a lower amount to assist with your cashflow. We suggest you contact your Mazars advisor to discuss this.

These tax planning ideas are of general nature only and have been provided to assist taxpayers with some general ideas in relation to their tax affairs. Accordingly, they should not be relied upon without seeking professional advice in relation to your own circumstances.

We also recommend you speak to your tax advisor about having your 2021 tax compliance prepared as soon as possible after 30 June. While the tax payable may not be due until 2022, early preparation will enable you to know any tax liability and budget for its payment. Alternatively, if a refund is due, it’s always better to receive this early and to reduce future PAYG Instalments by early lodgement of your return.

If you have any questions, require assistance or would like further clarification with any aspect of your end of year tax planning, please contact your usual Mazars Advisor or one of our Tax Specialists on the form below:

Brisbane – Jamie Towers | Melbourne - Evan Beissel | Sydney – Gaibrielle Cleary |

+61 7 3218 3900 | +61 3 9252 0800 | +61 2 9922 1166 |

* This is not a recommendation to make a financial investment, but a reflection of the tax attributes of such and accordingly should not be regarded as financial advice. Always seek professional advice from an AFS license holder before investing in any financial products.

Published: 17/06/2021

All rights reserved. This publication in whole or in part may not be reproduced, distributed or used in any manner whatsoever without the express prior and written consent of Mazars, except for the use of brief quotations in the press, in social media or in another communication tool, as long as Mazars and the source of the publication are duly mentioned. In all cases, Mazars’ intellectual property rights are protected and the Mazars Group shall not be liable for any use of this publication by third parties, either with or without Mazars’ prior authorisation. Also please note that this publication is intended to provide a general summary and should not be relied upon as a substitute for personal advice. Content is accurate as at the date published.

We are pleased to provide our superannuation year-end planning guide for 2021.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.